Same price, fatter tail.

A previous 10x shot doubled in potential, yet you can currently pay the same price as before. Calling all arbitration investors, where are you?

Imagine you hold a deep out-of-the-money call option. While you hold it, the upside scenario on the underlying doubles, the binary event acquires a confirmed date, and the issuer hands you back assets worth roughly 30% of your premium. You check the screen, expecting the option to have repriced.

It is trading exactly where you bought it 9 months ago.

Basically:

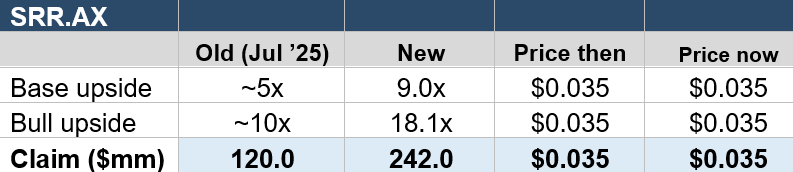

The damages claim doubled from USD$120-$242 million (now 26x current MC)

Management bought even more stock (now at ~16%)

Co just started divesting its assets (recent asset sales worth 30% of MC) to turn to a more pure play arbitration name

So what does the equity do?

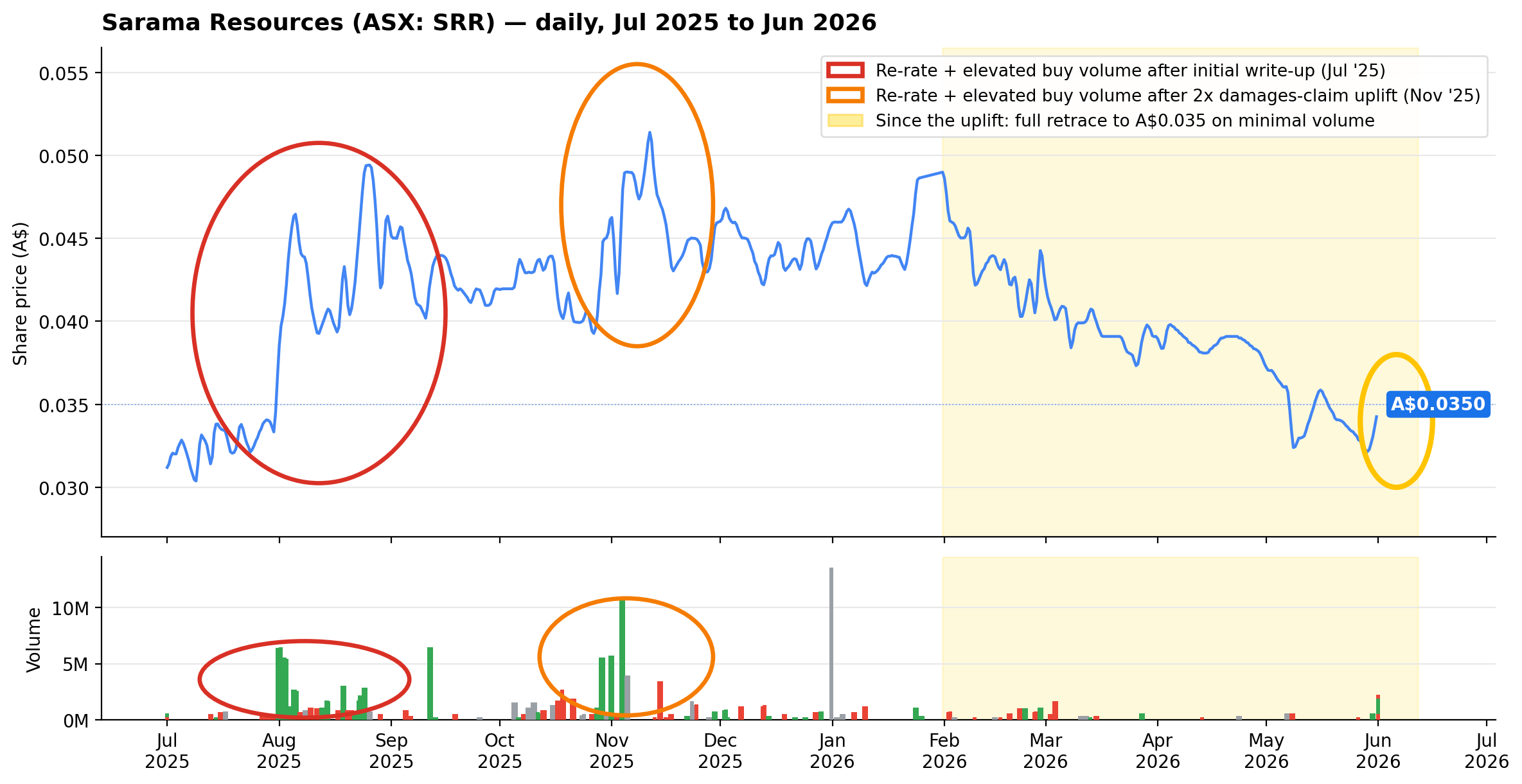

It rerates 30-50% of course, briefly, then comes back down to the price pre write up on tiny volume (shaded yellow).

Welcome to small cap land.

Name: Sarama Resources (ASX: SRR)

Current price: A$0.035

Market Cap: ~A$13 million

Est. upside: 5–18x across scenarios

I covered SRR in detail during my initial write up here.

The short version:

Sarama spent 12-13 years and roughly US$80 million developing the Tankoro gold deposit in Burkina Faso, only to have its permit withdrawn by the state in 2023. The company is now prosecuting a claim for unlawful expropriation before ICSID, the World Bank’s arbitral forum, under the Canada–Burkina Faso Bilateral Investment Treaty (BIT). The case is fully financed by a non-recourse facility from Locke Capital (specialist litigation financer) and run by Boies Schiller Flexner’s mining arbitration team under Tim Foden, a group whose recent record in materially identical permit expropriation cases stands at six wins from six attempts [IDA.ax, WIN.tsxv, MON.tsxv, LPK.tsxv, GRX.ax among them, with post-award equity returns ranging from +40% to +400% and successful awards from $30-$500million].

Damages claim 2x that of the original

Back in November, Accuracy London (the independent quantum expert) uplifted the damages figure from an USD$120 million to ~2x the initial estimate, landing at US$242 million. This memorial has been heard by the tribunal, accepted and BF have filed their counter memorial.

This is an extremely significant catalyst for the stock. So as I expected it re rates, buttt then comes back down over the following months on no volume…

The newly improved outcomes

Above is the new base/bull scenarios after the uplift in claim damages. I obviously like this idea more than the market (if there is even anybody watching this name) since I handicap the bull case at a much higher probability then the market is currently insinuating.

I can’t give too much credit to the market here though, there is no write ups on X or substack apart from my own.

Regarding fee estimates, 30% is a great average to assume but there isn’t a need for me to dive deeper into that here, it is conservative and I’m satisfied with it. I could go into the probable fee structure (it likely gives the litigation funder a min 3-4x on their money, pays them first, then SRR gets the rest) about a 30% flat fee happens to cover majority of likely fee outcomes anyway. The only time SRR gets screwed by fees is when the award is much lower than 1x their sunk costs, this really could only occur if the parties settle at that amount which is unlikely considering Sarama and its majority owners (management) want to be paid what they are owed.

To remind you all, these claim estimates are based off sunk cost multiples, which is what we’ve seen over and over with these awards (in relation to permit expropriation). The tribunal’s aim is to make things as fair as possible, so we often get awards handed out at some sunk cost multiple > 1x. This is because of the opportunity cost, risk, time and effort spent in development are taken into account when deciding upon the award. USD$242 million (AUD$338 million, or 26x the current MC) is about ~3x the initial sunk costs. This multiple would likely include interest too. Noting that SRR spent 12–13 years developing this asset before getting it unlawfully stripped.

Looking to previous precedent in similar merited cases: IDA, MON, WIN et al did not have assets anywhere close as mature and got awards handed down at ~1.7–2.7x. SRR’s project was the most developed out of all those names by a large margin. Thus, this claim amount is not just a “shoot for the stars, hopefully land on the moon” number, but it is a decent estimate of damages according to past precedent. Seemingly, the market has not accounted for this, even though it is the basis of SRR’s claim and it looks to be a very fair estimate of damages.

Here is Tim Foden, head lawyer at Boies Schiller Flexner representing SRR, speaking about how awards get paid using sunk cost multipliers. The example he uses sounds eerily similar to Sarama’s case…

The only explanation I could give for the current value gap would be this:

Often companies participating in ICSID arbitrations have much more complicated cases (not just permit expropriation) so other calculation methodologies are used such as NPV/FCF, to arrive at a quantum. However, tribunals are wary of handing out awards based on these numbers as lots of assumptions within the calculations are sensitive to estimates (think discount rate sensitivity etc). So, you often see companies going for a home run claim, e.g. $400 mill, and receiving just $40 mill. But again, this methodology does not apply to us here. Using sunk cost multiples as an estimator for damages is a much fairer number as there are nearly zero assumptions which are sensitive to estimates. For example, IDA was awarded roughly $40 million more than what they claimed for and received ~USD$120mil total.

SRR put USD$80 million into the ground for development. A decade later, BF tells them to go kick rocks and that they are the captain now. Well at a minimum, SRR could have earned the risk-free rate on USD$80 million for over a decade just that is enough interest to cover our entire MC currently. Hence, a large opportunity cost here. Therefore, if it’s proven that BF unlawfully expropriated its permit, it’s completely logical to assume SRR is owed some multiple of its sunk costs [which would involve a development multiplier and some interest rate above LIBOR for the opportunity cost]. That should give you guys a better picture of payoff dynamics in this arbitration name vs others.

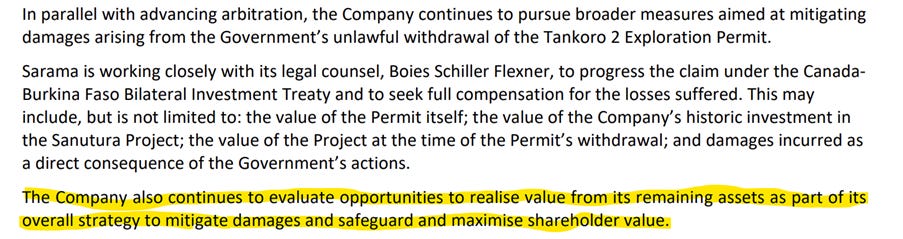

Asset spin off

"Hey Kingfish Capital, I like this idea but I'd rather be exposed purely to the arbitration option."

I got this a lot from the professional crowd. I would prefer there to be a market which values the arbitration case solely by itself too! While we don’t have that exact market per se, the equity is now much cleaner.

A few weeks ago, Sarama sold its WA gold assets to RIE.ax for 32% of the entire co (we get ~$4 million in equity, with our $13mill MC), rising up to 44% depending on performance milestones. SRR still holds the Bondi asset in BF, which I believe will keep until the arbitration is over for certain reasons pertaining to the case.

Just a reminder that the Bondi gold asset is likely worth more than the current MC itself. I will note that they are developing three early-stage small copper-gold tenements in NSW, Australia, where “the Company believes it can potentially add significant value for minimal expenditure”. We shouldn’t see any more dilution until we get an award handed down, which should take roughly 1–1.5 years from today assuming no settlement in the meantime. The Co also mention a bit of asset clean up(y) language in their Q1 2026 results notes.

In my initial post, I mentioned this case might result in a summary judgement due to Burkina’s silence on appointing a chairman to the case. Sarama have been a bit quiet on updating investors but looking at the ICSID site, you can see that Burkina have replied/filled its counter memorial and the arbitration is going ahead. Due to their late reply, BF did not get to choose their own arbiter to join the tribunal and instead had one appointed on their behalf. The merits hearing is from the 22nd of February to 26th of February 2027. After the hearing, ICSID cases take 6-8 months to hand out an award (new rule they’ve implemented). So, we have just about a year until we get colour on the award.

So, we have:

A memorial filed with 2x the original quantum estimate which heavily increases the value of a right-tailed outcome

The co starting to spin off its remaining assets (spinning off $4 mill in assets is meaningful when your MC is $13 mill),

Management buying even more stock (~16%) and participating in all the CRs, Burkina Faso filing a counter-memorial locking them into defending the case (no reneging on the BIT treaty signed back in 2017) and a sharp increase in the price of gold increasing BF’s ability to pay.

All of these positive catalysts, yet here we are at the exact same price we were before any of this was known…

In my previous article I wrote:

”From being involved in so many past ICSID cases, I always found it important to watch price action… simple catalysts like memorials being filed, the starting of hearings resulted in price moving up even though these events were known to happen roughly around those times… goes to show these situations simply aren’t priced correctly.”

I believe this is one of those situations.

The value of a “free look”

A free look, or “free roll”, holds immediate value due to optionality “taking up” some amount of worth. I really liked Sarama as a mega undervalued/right tailed call option back when none of these catalysts had occurred yet, so naturally, after the positive catalysts eventuated and the price stayed the same, I have now re-bet. If you employ this same sort of framework over your investing career and let situations play out over time (win or lose), I think it’s likely you will come out on top. That’s just what happens when you can constantly get set in situations where you receive positive information and then have the opportunity to bet or not bet, assuming price stays the same. By definition you come out on top if there’s enough trials but you have to be certain of your edge. This is just a long way to say: with all the positive news flow and circumstance, I believe that at the current price, SRR equity represents a positive expected value bet and a seriously underappreciated/niche trade.

Disclaimer: NFA, DYOR. I own shares of SRR.ax and may buy/sell at anytime.

It's an interesting play but the main risk to the thesis is enforcement against a country like BF. This is not the same as the Ascent vs. Slovenia litigation (should be decided in weeks, as no doubt you know!) where the counterparty is a civilized EU country that generally plays by the rules of law and so full award payment is a realistic scenario after some initial foot-dragging. Getting the thugs that rule BF to pay anything? Good luck with asset seizures - BF is a dirt poor s__hole that probably has very few assets around the world that could be confiscated or they will be protected by immunity doctrines (you can't go and seize an embassy building). It's not a commodity-rich country to whom you can just confiscate a tanker full of oil or a bank account where oil sales end up. If the award is good (and it should be, considering that BF filed late, doesn't have their own arbitrator and their case is likely quite flimsy), there will no doubt be a violent re-rating of the stock on the award, but I also think it will be significantly discounted compared to the award face value. Sarama's best plan will be just to take the award receivable and offload it to a specializer enforcer who will probably spend years chasing BF thugs' assets around the world. There will be a significant hair-cut though, likely 30-50% of the award value, on top of what you already have to pay your lawyers for winning the litigation in the first place. When you model this secondary haircut, my modelled upside is closer to 5-7x. 10x is imho too bullish but what do I know. I am just a fool talking to my buddy Claude a lot.

Do you know what's up with the cosmo newberry exclusion zone? Thanks