A completely unknown arbitration case offering 10-15x upside with full downside protection.

I’ve found a goldmine (pun intended) that offers a 10-15x free call option in an arena i’m extremely familiar in, with downside nearly fully protected downside via forgotten assets.

Kingfish Capital is emerging from hibernation for what I believe the most compelling risk/reward setup I’ve seen in the ICSID arbitration universe and arguably one of the most asymmetric special situation in public markets right now.

Sarama Resources

Ticker: SRR.ax

Market Cap: AUD$12 million

Upside: ~10-15x

Catalysts: Multiple near-term

Here at Kingfish Capital, we (it’s just me lol) like upside as much as the next guy. But I do things a little differently. Making 10x your money is great but how much risk did you take? You see, the thing about risk is you don’t know where you sit in the sequence of those probability affected outcomes. Believe me I know, me and variance very are well acquainted with each other (it’s a one sided relationship). You can play a hand of blackjack, hit 21, leave and say “Boom” all you like but what if that bet lost? Are you going to bet again? And say that hand wins, but then the next 5 hands in a row lose, now what? This is why we need something more then just an opportunity to “bet”. As is why today, I present you with Sarama Resources (ASX: SRR), a blackjack hand where we get paid $10-15 per $1 stake when we win, but only forgo ~$0.3 when we lose. Essentially giving us leverage in the form of astronomical positive expected value.

Sarama Resources presents a rare, deeply asymmetric special situation opportunity anchored in an international arbitration process under ICSID jurisdiction. An opportunity that not only is yet to be priced in, but one I am extremely familiar with. The company’s core asset, the Tankoro 2 gold project in Burkina Faso, was seemingly expropriated by the Burkina Faso government. After a decade of development, Burkina Faso illegally withdrew Sarama’s permit to continue the activities needed in order to round out the full development. Luckily, there are protections in place for situations like this, and we can profit off them.

Background

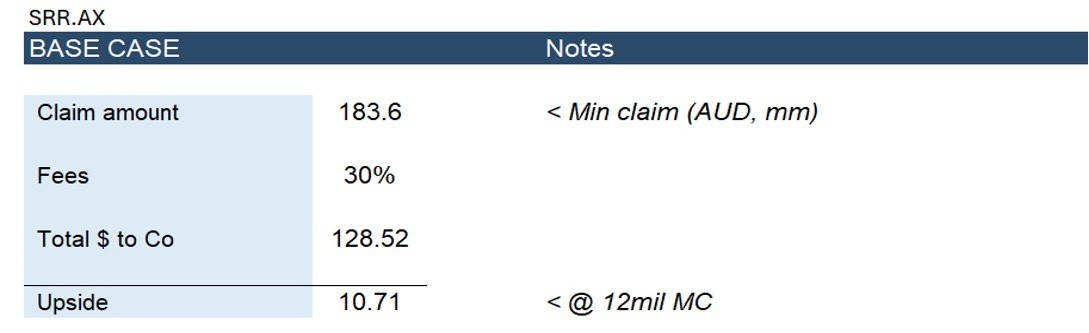

As a surprise to absolutely nobody countries can’t just render assets useless (here, through the proxy of a permit) when there is no reason to do so under treaties they are legally binded to. This is why Sarama is pursuing compensation for damages of minimum US$120 million (AUD$183 million, $12mil MC) under the Canada-Burkina Faso Bilateral Investment Treaty (BIT) which was signed by Burkina Faso in 2017, supported by specialist litigation funders and top-tier international legal counsel who are currently 6 from 6 in ICSID cases with the same precedents. (see IDA.ax, WIN.tsxv, MON.tsxv). I have also been involved in the aforementioned names.

Forget the fact that this is a sold-down nanocap with the complete wrong register. Forget that ASX investors don’t understand ICSID claims or value legal optionality whatsoever. Forget the fact the company hasn’t bothered to educate their shareholder base on the very real chance of a large award being paid out. There is more to it than just a massively discounted call option style play. I also believe I have an edge on a few of the upcoming catalysts too.

Edge

I believe there is a good chance the independent quantum report (which will be completed soon) will include a number bigger than that of the current conservative number posted by the company. If it does, this will result in an immediate re-rate.

Let’s look at the facts, IDA.ax was awarded 1.7x sunk costs, WIN.tsx was awarded 2.7x sunk cost (these are the cases with the exact same precedent AND lawyers as as SRR.ax).

SRR.ax has posted a 1.5x sunk cost figure as the minimum for their claim… In IDA and WIN, they both earned 20%+ of their claim in interest costs. LIBOR + 2% rate would likely be used like in the other cases which would result in a 1.7x sunk cost figure for SRR if the case was seen out for the average 3 years.

However, sunk cost multiples are given out depending on the development of the asset. IDA.ax didn’t even develop their project, they bought it. Sarama spent 12-13 years developing, starting out from grassroots exploration. They spent ~USD$80 million (AUD$121 million) in the ground, for the development of the Tankoro 2 deposit asset. Remember, litigation finance has already been provided, the lawyers have already completed their extensive due diligence, so the 120mil USD figure SRR spouts as the minimum claim amount, really is going to be the minimum claim amount.

Therefore in my opinion, there is a good chance the independent quantum report is likely to report a figure above the 120mil USD figure and trivially this would result in a re-rate in the equity price.

This is not the only thing I found.

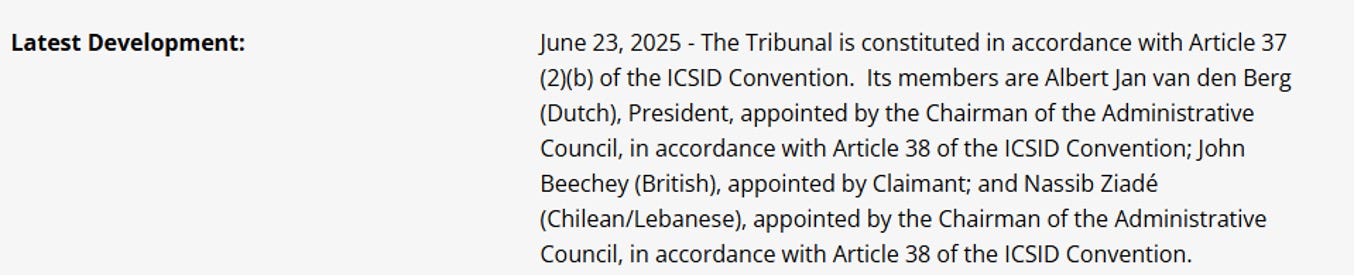

In ICSID cases, one tribunal member is to be appointed by the claimant, one by the defendant and one by the Administrative council in order to remain impartial.

Now, looking at this dense bit of text on the ICSID website we can see that it states as of June 23, 2025 - “Nassib Ziadé (Chilean/Lebanese), appointed by the Chairman of the Administrative Council” – If you read the whole paragraph you will notice that one arbiter is appointed by the company, one by the tribunal and one by the defendant Chairman? This means that Burkina Faso has not appointed their own arbiter, and therefore have not been a part of the ICSID process so far. Burkina Faso also failed to engage during the mandated 60-day consultation period following Sarama’s Notice of Intent to Arbitrate in November 2023, which insinuates no engagement at all. This is a positive, it means that there is a much higher chance of a default judgement (Under Rule 49), a default judgement usually means an outcome much faster than otherwise. It also means Burkina Faso would not have the ability to provide evidence for their defence, increasing the likelihood of full payment from the independent quantum report claim dollar figure (Min USD$120mil).

You’re probably wondering, “But if Burkina Faso don’t participate in the arbitration, how do we get paid out?”. Well first things first, specialist arbitration lawyers and litigation financers don’t just throw millions of dollars at things in “the hope” of an outcome. Many cases come across their desk and they need to be extremely selective (so they can make a living). What happens in this scenario is we move to the enforcement procedure. This involves - legally (as per the BIT agreement signed in 2017) - taking Burkina Faso’s assets which are in any of the ICSID members countries up to the amount of the claim value. This is also budgeted for within the litigation finance. They have billions in central bank reserves held within other countries and billions in other foreign assets. The details on what assets they own and where isn’t important for me, as the due diligence here has already been completed for us. Remember that ICSID is a division of the world bank and we’ve seen them provide large amounts of $ for example when Tanzania was getting hit with heavy award payouts from ICSID. But please don’t worry about the possible enforcement too much, it’s important to understand the level of due diligence the parties fighting the case had to take on before committing to it.

From being involved in so many past ICSID cases, I always found it important to watch price action. Every time simple catalysts like memorials being filled, the starting of hearings etc resulted in price moving up even though these events were know to happen roughly around those times. Just goes to show these situations simply aren’t priced correctly.

But it gets even better.

Sarama is currently at a $12 million market cap. Min award payout after fees sitting at a rough min ~10x from current prices. I know what you might be thinking, what if they lose (though like IDA, there just isn’t a strong case for a loss but lets get into it). What if there is a technicality the lawyers missed or what if the lawyers and funders are just “swinging for the trees” and hoping to hit it big while the real chance of a win is small?

So lets see, Sarama has nearly ~$3 million in cash to fund its current assets (qtr of MC) but it also has other assets. Big assets that may have been lumped into the wrong basket by investors.

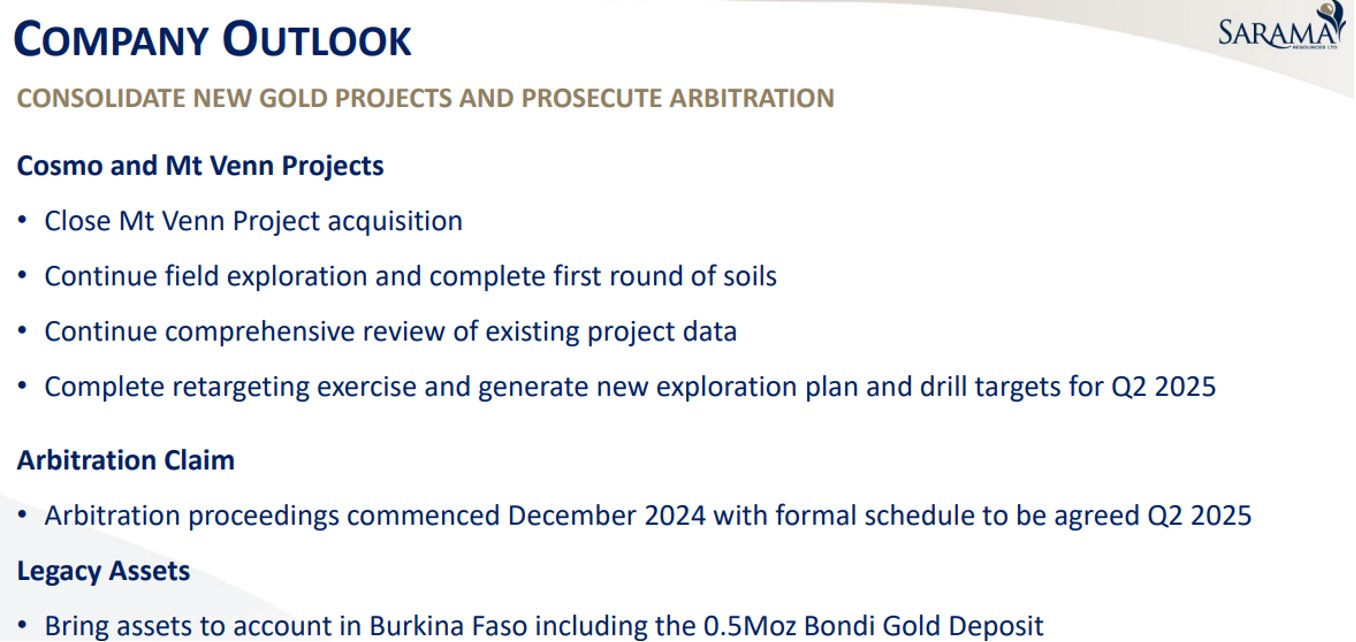

Back in Feb this year Sarama announced they wanted to sell their other assets in Burkina, including the 0.5Moz Bondi Gold Deposit. Now they have not mentioned it since, probably due to the current case with their Tankoro 2 asset but I believe there is also optionality on the sale of these assets.

Disclaimer, I know nada about commodities and even less about the value of them within an African geographic. Doing light research, the Bondi asset alone could be worth US$10-40/oz conservatively (using conservative comps for geographic + inferred ounces). Let’s use the lowest end. That would put Bondi to be worth AUD$7.5 million (MC is 12mil and there is 3mil cash…). You’re welcome to discount that further but I do not believe you can put this asset to be worth 0 (I welcome collaboration on the calculation). There definitely is PE interest in gold projects still in Burkina, see here and here. The reason why they don’t just steal assets willy nilly is they need to seem like a semi investable geographic. Signing the BIT treaty in 2017 is proof of this.

Sarama just did a capital raise of $2.7 million, the offer was initially for 2 million and was heavily oversubscribed. They have costs of $900k/year AND are fully funded with a $6.7million non-recourse loan for the arbitration (via specialist funders Locke Capital). In other words, expenses are well and truly covered and accounted for, there should not be any further dilution at all while we wait for the outcome of this arbitration.

To reiterate, the lawyers involved just came off the back of 3 from 3 wins with cases of the same precedent, this company already trades at a large discount to its assets, it’s fully funded to see the arbitration out/for working capital and it’s possible we get the entire arbitration option for free (with 10-15x upside attached) via a sale of the old assets. In any way you look at it, I have to be involved here.

Why would Burkina Faso do this?

Well, apart from the countries upstanding reputation (uhhhh), it’s actually the right decision game theory wise. If they can steal 3 million ounces of gold worth a cool “billy” in NPV but pay the company out in a settlement worth 100 million, they’ll take that, make the difference, and be on their merry way. I’m sure in their mind that’s fair business. Many African countries operate this way and it’s why geographical discounts exist.

This fits in with the nation’s current plans (here) to nationalising more gold projects from western mining companies and make a motza from the gold resources. In short, they do it just because they can. They have also benefited greatly from this recent gold run, gold flew from US$1940 in 2023 to $3,347 in 2025. It’s reported that Burkina Faso has made US$18 billion in gold related profits since 2022 when Traoré took power…

Settlement before the hearing is also a possibility however (I believe this is what both parties will push for, even in the reality of Burkina’s current radio silence) we need to remember the kind of country we are dealing with here. Like for IDA.ax, WIN.tsxv and MON.tsxv, in these African countries domestic laws are somewhat of a facade that aim to keep the society civilised. In short, they need to be seen being strong, handing over $180mil while majority of its people are below the poverty line can result in some not so good things happening to those leaders. It is no joke in these jurisdictions, lives would be at stake. But let me tell you, this has no bearing on the legally binding ICSID outcome. I watched all of the WINS.tsxv hearing. The arguments made by the defendants (Tanzania in this case) were so laughable that not only did the lawyers physically laugh, but the arbiters let out a few chuckles too. It was like they were making up some of this stuff on the spot. Not a joke, I doubled my position after. They unsurprisingly won and the award was handed down in record time.

The upside

First thing to note is the financing terms. The truth is we don’t know the exact fees of the litigation funding. But the $6.7 million non-recourse loan insinuates a competitive process (it’s a great deal). No win and Locke Capital makes $0. Litigation funders usually take a multiple of the provided finance or a flat fee. The multiple averages around 2-4x. However, there is obvious nuance in settlement situations and lower award amounts. What is conservative is to assume a 30% flat fee and I have no issues saying that is a good estimate.

Now lets talk about the lawyers. Let’s just say Tim Foden and his international arbitration team are no joke. These guys have found a little goldmine (pun intended) for themselves here. Seemingly, it looks like they only take on cases where they are likely to get paid which makes sense because they work on a no win no fee basis. From their past cases it looks like they basically only take on situations where a mining permit was expropriated/not renewed unlawfully. They take on months of due diligence looking at internal emails, models, meeting minutes, past precedent, hiring of their own independent quantum expert for award size estimate, and enforceability. They CANNOT afford to be wrong and their track record shows it (6 from 6 with precedents the same as SRR).

Here’s the leading lawyer Tim Foden speaking about these mining arbitration claims including SRR, posted just last week.

Sunk cost multiples of 1.5-2 resulting in upside of 10x-14x. Be mindful that a settlement is also a possibility though I can’t see Sarama wanting to take too much of a haircut considering ~US$80 million is 1x sunk costs. Even a settlement of 30c on the dollar of just 1x sunk costs provides upside of 5x (at AU$12mil MC and accounting for fees). Hence, the right-hand tail upside on this situation is extremely long.

Incentive alignment for the upside

Management also own 15% of the co and subscribed for the max they were allowed in the recent capital raise (~$120k with entire cap raise @ 2mil, ending at 2.7mil but 4mil of interest). They want the best possible outcome in this arbitration too and considering our interests are all aligned here, I believe obviously they would push for the best outcome regarding settlement.

Why does this opportunity exist?

Well, I’ve seen sophisticated private investors make a thread on twitter about insane value in small caps and the next day the stock is +40%, gap is majorly closed, and the price stays there (showing the price discovery). I’ve seen other small cap stocks get indiscriminately sold 20% in a day due to a fund’s liquidity issues (as announced by the company themselves) and that stock staying -20% for days and days, on exactly ZERO other news and then preceding to close the gap all in one trading day.

What I’m trying to get at is, what do you expect from an 12mil MC junior gold mining company that got their main asset taken away from them 2 years ago and is left with a couple other small gold assets and some cash. In these ICSID case related equities you could drive a truck between the true price and the current price due to the visibility issue. Especially because this trades on the ASX, there isn’t much knowledge on the situation (I couldn’t find one write up or mention about it online/fintwit and I’m not surprised). The company itself has also barely mentioned it or bothered to educate its investors. The investor base is simply punters who want drilling results, not crafty special situation investors who look for stuff they can pay ~A$1–2M of market cap exposure in exchange for equity in an award claim potentially worth A$150–300M.

Sizing

So sure you can treat this as call option in the form of an equity, throw it in your PA and wait until the final outcome but I don’t believe that would give you the most edge. Considering I believe I have an edge in upcoming catalysts (but also at the current px regardless), for me, the right trade is to stake high FIRST, cut on catalyst, and then hold a position size that would similar to a call option. Though, the end stake actually needs to be higher then what i’d stake on an actual call option since there is optionality of having no strike nor expiry. It is also non zero-sum situation (due to current assets, possible sales) meaning you can stake more and lose less (in event of a loss) to that of an actual vanilla call option. This is how I think about staking.

The stock also trades on the Toronto exchange under ticker SWA.tsxv too if you’d prefer to buy there. Liquidity is limited.

Disclaimer: NFA, DYOR. I do own shares of SRR.ax and will buy/sell as I see fit.

Hell yes, this is fantastic work and exactly the kind of investing I love. Buffett would be proud. Now can you please take this down so the price stops going up while I'm trying to research it lmao

From what I can tell, everyone involved in the arbitration is very experienced indeed. Together with the fact that BF didn't send an arbitrator, this case might finish in record time. Record time would be 12-18 months. I'd expect 18-24.

I expect them to win and be awarded not a lot more than the A$180M Sarama sues for.

If you assume they get paid what they are awarded and take a very healthy haircut, this is a good buy, very high double digit returns p.a.

I am not sure at all how likely it is BF will pay or be compelled to pay, or have its holdings seized. By default I would assume BF does not pay, but maybe they have an incentive, like wanting/needing foreign capital, or need to polish their image as a reliable country for negotiations. I really have no clue about Burkina Faso, so off to researching.

If you have an opinion about or experience with/in BF, please do comment.