New position - Carnarvon Energy (CVN.AX)

Piggybacking on activist investors. 100%+ upside.

Overview

MC: A$350 mil

Current price: $0.18

Target: $0.35 or 100% upside.

Average daily volume (ADV): $400-$500k

Position: 437,048 shares @ $0.175

Carnarvon Energy, an Australian oil and gas company with a market capitalisation of $290 million AUD and is significantly undervalued with value unlocking catalysts due to shareholder activism occurring soon. The company’s stock, last price 16 cents, is trading at nearly a negative Enterprise Value, which is remarkable considering CVN's notable involvement in Australia's Dorado discovery, the most significant oil and gas find in the country in the last 30 years.

The situation

I’m not going to try value CVN myself as its not my competitive advantage, you’ll see an activist investors valuation below. But for the last few months you could buy CVN equity below net cash, and get significantly valued Oil and Gas assets (hundreds of millions of $, remember MC is just $350 mil) for free. So simply if you sell the main assets and return capital to shareholders the upside is 100%+. This is what we want to achieve.

The activist shareholders

Nero Resources: A notable entity in this context is Nero Resources, a Perth-based investment firm specializing in mining-related investments and activism. Nero has a history of effective activism in similar companies, demonstrating both the willingness and capability to instigate significant corporate changes. Their approach often involves advocating for shareholder interests, challenging inefficient management practices, and pushing for strategic revisions that can enhance company value. More about him below. Nero manages $145 million, and holds 5% of CVN hence, has approximately ~10-11% of his entire fund in this equity.

Other activists: Apart from Nero, Collins St Asset Management (special situation and value fund) and Jeremy Raper (full time private investor, see his post here) are going activist on CVN. Both of these groups have been significantly involved with other shareholder activist situations, they know what they’re doing.

As a result, the board has recently split and 2 independent executives hired by Nero and Collins St. The first, Russell Delroy the CEO of Nero Resource fund and the second, takeover experienced geologist William Barker.

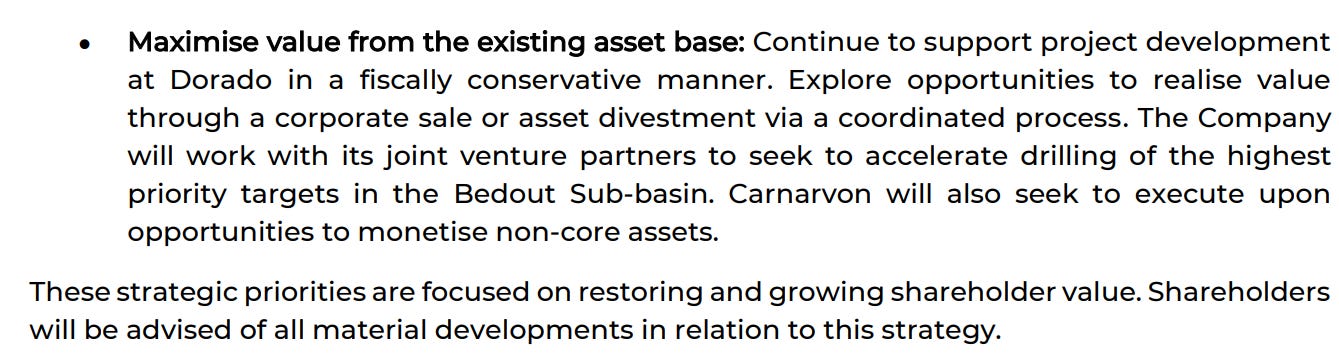

This outcome is as favourable as we could have anticipated. The announcement emphasized the preservation of the cash balance (with a clear directive against acquisitions), the reduction of General & Administrative expenses (G&A), ensuring that the free cash flow remains neutral prior to exploration expenses, and that any decrease in G&A spending is compensated by interest income. Additionally, the statement indicated a comprehensive evaluation of all possibilities for asset monetization. The pivotal aspect here is the explicit pledge to safeguard the cash balance, effectively removing downside risks. Here is what CVN said explicitly,

In terms of activists situations, this seems like one of those high probability situations to be successful.

Also, at the AGM this year the remuneration package received its “first strike” with >25% of the registry voting against the decision. This means if this 25% threshold vote is met again at the next AGM (which it will if CVN do not follow the plan to maximise shareholder value) then the activists can spill the board.

I personally wont be trying to value CVN myself due to my lack of experience in commodities instead, here is one of the activist’s sum-of-the-parts calculation of CVN’s equity instead.

Source: Jeremy Raper’s twitter post

I concur with Jeremy that this SOTP calculation is pretty conservative, i’ll be using 35c as my price target. If I was to change something, I’d up G&A costs as I think it takes a little longer to reach 35c and lower interest income a smidge to discount for the fact excess capital may be largely returned to shareholders within a years time.

Its important to note that I did not find this situation myself and in fact I rarely find investments myself, its usually off the back of an idea I see. Valuation is also not my competitive advantage. But I can still follow on someone else’s analysis easily, and I love the conservative estimates being used here.

Position sizing

The MC is ~70-80% in cash, a great margin of safety. There are multiple motivated activists. Very minimal downside risk now. However, timeline of value unlock is unknown so I’m going to have to give this a timeline of 1.5 years.

Considering all of these factors, even with such a long timeline, this situation warrants a large position size. I’d say this situation likely has a discounted IRR of 50%+ due to the minimal downside + small probability of downside and large upside (100%+) + large probability of upside. Hence, I am putting 15% of my total portfolio in this

.

Any change in the thesis with recent pullback?

https://www.energy-pedia.com/news/australia/canarvon-energy-provides-dorado-update-196821